1 引言

然而,当下中国的经济全球化发展道路依旧存在诸多不确定性,一方面,中国与以美国为代表的发达国家间的经贸合作和竞争关系正发生深刻变化,两股力量间的复杂博弈将逐渐常态化;另一方面,其他发展中国家对经济全球化的各种利益诉求相互交织,但缺乏有效的全球治理机制予以响应,全球经济治理面临全新形势与挑战。特别是2020年新型冠状病毒肺炎疫情(简称“新冠疫情”)的全球爆发,给世界各国经济带来巨大冲击,由此引发世界各国政府对于未来经济全球化发展道路的再思考,更是给未来中国的经济全球化道路增添巨大的不确定性。因此,准确认识中国在当前全球化浪潮中的角色转变和原因具有重要的理论和实践指导意义。现有政治学、经济学和国际关系等学科的相关研究多以全球经贸发展过程中的生产组织变动为主要切入点来论述中国应如何在经济全球化中实现角色转变和升级[7,8]。然而由生产组织变动所带来的世界经济地理格局的演变却较少为这些研究所关注。随着近年来各类区域性贸易联盟的形成和发展中国家的逐渐兴起,经济全球化中各尺度地理空间中经贸互动越发复杂多样[9]。因此,从空间视角对上述问题进行剖析或能进一步丰富对经济全球化变革中中国角色演变的认识。

2 经济全球化变革下的世界经济地理变化

2.1 经济全球化三次浪潮

本文将经济全球化过程划分为三次浪潮。第一次浪潮发生在始于18世纪中的第一次工业革命时期,英国和法国等率先工业化的国家成为第一次浪潮的主要推动者。在此背景下,以发达国家提供工业制成品、发展中国家提供原材料和初级工业产品的核心—边缘式全球经济网络逐渐形成[10]。虽然各国间因劳动生产率差异而互有分工,但是这一时期大部分生产制造活动依旧囿于国家内部,生产活动的全球化水平较低。因此,第一次浪潮期间世界经济地理格局的主要变化是贸易全球化程度大幅提升。

20世纪50年代,第三次工业革命的到来开启经济全球化第三次浪潮。在这期间,生产要素的跨国运输成本大幅度降低,为生产活动在全球布局提供技术可能。20世纪70年代西方发达国家普遍出现的“滞胀”危机加速第三次浪潮的发展进程。为缓解“滞胀”危机,西方发达国家政府采纳新自由主义的政策主张,给予企业更多进行跨国投资和贸易的自由[13]。在制度性变化和技术进步两股力量的共同作用下,跨国企业开始在全球范围内寻找合适的区位进行产业转移。

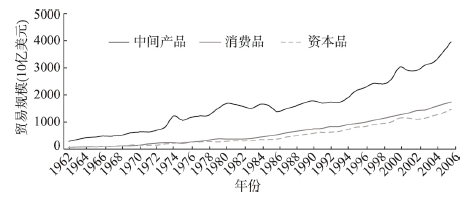

图1

图1

1962—2006年各类型产品全球贸易情况

注:数据来源于联合国贸易和发展会议(UNCATD)。

Fig. 1

International trade by product type during 1962-2006

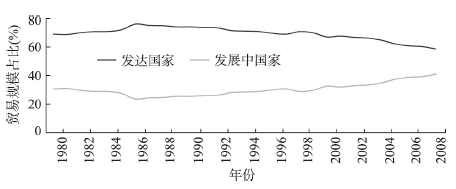

图2

图2

1980—2008年发达国家与发展中国家全球贸易规模对比

注:数据来源于联合国贸易和发展会议(UNCATD)。

Fig. 2

Share of developed and developing countries in international trade during 1980-2008

从国家层面来看,发展中国家在全球贸易网络中整体发展水平的提升主要来自于中国和印度等新兴经济体的崛起。1998—2018年美国、日本和部分欧洲发达国家的对外贸易份额不断下降,其中美国下降幅度最为明显,从15.65%下降到了10.83%,欧洲发达国家普遍下降了2%左右。与此同时,中国对外贸易份额上升趋势明显,1998—2018年中国对外贸易份额占全球比重从4.21%上升到12.34%,成为全球最大贸易国。相比之下,在非洲、拉丁美洲和大洋洲等地区,大部分国家都长期维持在较低的占比水平(表1)。

表1 1998—2018年各地区对外贸易占比(%)

Tab. 1

| 国家 | 1998年 | 2002年 | 2008年 | 2018年 | 1998—2018年变化 |

|---|---|---|---|---|---|

| 中国 | 4.21 | 6.20 | 8.67 | 12.34 | 8.13 |

| 印度 | 0.62 | 0.80 | 1.49 | 1.83 | 1.21 |

| 美国 | 15.65 | 14.69 | 11.06 | 10.83 | -4.82 |

| 日本 | 8.28 | 6.06 | 4.66 | 3.88 | -4.40 |

| 德国 | 9.48 | 8.58 | 7.63 | 7.30 | -2.18 |

| 英国 | 5.28 | 4.89 | 3.49 | 3.06 | -2.22 |

| 法国 | 5.53 | 5.06 | 4.04 | 3.43 | -2.10 |

| 意大利 | 4.15 | 3.80 | 3.34 | 2.81 | -1.35 |

| 拉丁美洲 | 2.83 | 2.27 | 3.31 | 2.89 | 0.06 |

| 非洲 | 1.83 | 2.07 | 3.21 | 2.68 | 0.85 |

| 大洋洲 | 1.63 | 1.40 | 1.61 | 1.68 | 0.05 |

注:数据来源于联合国贸易和发展会议(UNCATD)。

2.2 从全球价值链的渗透到网络不均衡

全球贸易规模的快速增加并不意味着发展中国家在全球产业分工体系中的边缘地位得到明显改善[16]。因为价值链分工体系的不断渗透,全球经济网络中产生了新的不均衡,发达国家在高新技术产业方面发展能力不断提升,而大多数发展中国家的本土企业则被长期锁定在低技术水平的制造生产环节,只有韩国、新加坡等“亚洲四小龙”地区中的少数企业在政府的扶持下得以脱颖而出,实现技术创新和高水平升级。

21世纪以来,在长时间的网络不均衡下,经济全球化第三次浪潮中存在的问题也逐渐暴露出来。在发达国家劳动密集型产业的迁出造成内部制造业的“空心化”。在发展中国家,长期处于全球产业分工体系的低端地位使得其发展速度日趋放缓甚至下降[23]。而这一系列矛盾在2008年金融危机的爆发之后变得尤为突出,使得世界各国政府开始对经济全球化进程进行重新思考,经济全球化第三次浪潮开始出现变数。

部分发达国家为缓解本国制造业就业压力,制定了相关政策吸引本国制造业企业从欠发达地区向本国及其周边地区回流,例如美国的“重振美国制造业”系列产业政策。与此同时,得益于数字信息等技术的进步,服务产品的可贸易性大大提升,为了规避国内由于金融危机带来的风险和监管力度的增加,原本集聚于发达国家核心城市的高级生产性服务业开始向欠发达地区的核心城市进行迁移[24]。在两股浪潮的作用下全球价值链的空间渗透格局出现了与前一阶段相异的趋势,低端环节开始向发达国家回迁,而高端环节则开始离散化的全球分布。

同时,发展中国家对待经济全球化的方式也开始发生转变。一方面大量跨国企业建立的工厂关闭或迁出让发展中国家开始意识到被动和边缘化地参与经济全球化所存在的问题,由此开始主动寻求构建生产网络的机会和方式。另一方面,发展中国家间日益紧密的经贸联系和共同的利益诉求使得其开始主动寻求经济全球化的新可能。在此背景下,2013年由中国发起的“一带一路”倡议应运而生,并获得其他发展中国家的广泛响应,开启由发展中国家共同主导的经济全球化新道路[6],经济全球化的主导力量中也开始出现发展中国家的身影。

综上,在经济全球化第三次浪潮中,无论是前期的生产全球化阶段还是后期的发展中国家对经济全球化集体再思考的阶段,中国不仅都扮演着重要的角色,还实现了从参与者到变革者的角色变迁,而这一角色变迁成为本文下一部分讨论的重点。

3 中国的全球化角色变迁:从梯度转移到网络嵌入的路径重构

3.1 全球产业转移的空间秩序与中国角色

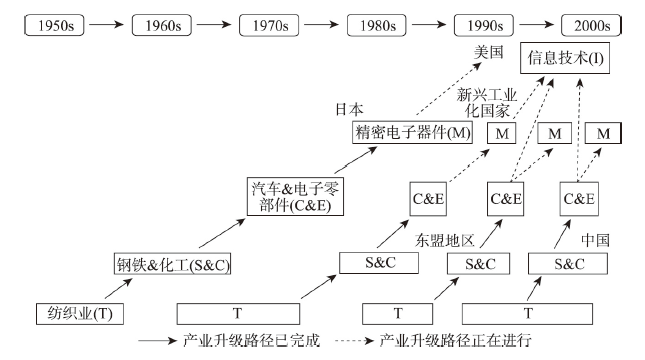

第二次世界大战结束以后,欧美发达国家产业化迅速发展。随着低端制造业在发达国家本土的生产成本不断上升,产业竞争力开始下降,发达国家开始将劳动密集型产业大规模地转移至低成本国家和地区。形成如图3所示的梯度转移式的空间秩序。1950年日本率先成为欧美等国的纺织服装和鞋帽等劳动密集型产业的承接地。随着日本生产技术的进步与提升,同时劳动力和土地资源供给不足等问题的出现,日本也走向产业转移的道路。一方面开始向东亚的其它国家转移其劳动密集型产业,另一方面专注发展钢铁、化工等技术密集型产业。随后日本再次发生产业转移,将这些技术密集型产业中的劳动密集型环节转出到东亚其他国家,自身专注于发展精密电子等高科技产业,而此时发生多轮产业转移的美国已演变出以互联网技术为核心的产业结构。这种产业转移的梯队依次在韩国、新加坡等区域传递,直到19世纪80年代,中国实施改革开放,大量的劳动密集型产业转入中国,但此后40年至今,大量的劳动密集型产业在转入中国之后,尽管外商直接投资速度日渐放缓,但尚未发生新的大规模跨国产业转移[25,26]。

图3

图3

20世纪50年代—21世纪初跨国产业转移梯队

注:根据Liu[26]研究中

Fig. 3

Sequences of global industrial relocation, 1950s-2000s

表2 1998—2018年中国外商直接投资规模及主要行业分布

Tab. 2

| 指标 | 1998年 | 2005年 | 2008年 | 2018年 |

|---|---|---|---|---|

| 总规模(万美元) | 4545300 | 6032500 | 9239500 | 13496589 |

| 制造业占比(%) | 56 | 70 | 54 | 31 |

| 生产性服务业占比(%) | < 5 | 8.82 | 10.73 | 34.12 |

| 租赁和商务服务业 | - | 6.21 | 5.48 | 13.98 |

| 金融业 | - | 0.36 | 0.62 | 6.45 |

| 科学研究、技术服务和地质勘查业 | - | 0.56 | 1.63 | 5.05 |

| 信息传输、计算机和软件服务业 | - | 1.68 | 3.00 | 8.64 |

注:数据来源于国家统计局;1998年生产性服务业数据未披露,所展示数据根据已披露数据计算得到。

然而,与2008年之后制造业占比逐年下降的趋势不同,以金融业为代表的生产性服务业外商直接投资占比则呈现不断上升的趋势。虽然也受到了金融危机的冲击,但是由于中国金融系统对外开放程度相对较低以及中央政府宏观调控的积极作用,使得在金融危机冲击之下中国宏观经济发展环境依旧保持相对稳定[28],稳定的金融发展环境成为了中国吸引生产性服务业进入的重要原因。2008—2018年中国生产性服务业吸收外商直接投资的规模增加明显尤其是金融业。2018年生产性服务业吸收外商直接投资的规模已经超过制造业,占到了总投资额的34.12%。中国吸引外商直接投资的质量显著提升,表明中国在全球产业分工的角色逐渐多元,不再仅仅只是承担外围的低端制造职能,也开始逐渐承担起核心区的管理和研发职能。

中国在全球产业分工体系中地位的多元化提升不仅仅只是依靠吸收外商直接投资质量的提升,还得益于大量优质中国企业开始通过对外直接投资主动构建全球产业分工体系。从时间上看,中国企业的大规模对外投资始于2008年,当时生产成本上升的压力使得中国势必将再次走向通过对外投资转移劳动密集型产业来为本地新兴产业发展提供空间的产业转移路线。然而,本文发现中国对外投资并不是对传统全球产业转移空间秩序的简单复制。相比之下,中国企业主导的国际产业转移表现出一些新的特点。

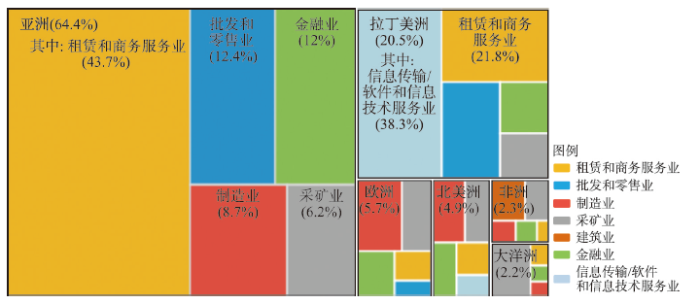

首先,区别于以往全球产业转移过程中对外投资空间格局的相对集中,中国对外投资表现出空间更为分散的特点,截至2018年,中国企业对外直接投资已经覆盖了全球80.34%的国家和地区,尤其在亚洲、欧洲和非洲等地区覆盖率较高,分别达到95.83%、87.76%和86.67%。其次,中国对外投资所涉及行业领域呈现多元化特点,中国对外投资的主要领域并不局限于制造业。整体来看,中国对外直接投资主要集中在租赁和商务服务业、批发和零售业以及信息传输/软件和信息技术服务业。在不同区域,中国对外投资的投资重点也有所差异,在亚洲主要投资于租赁和商务服务业、批发和零售业以及金融业。对拉丁美洲的投资主要集中于信息传输/软件和信息技术服务业。在欧洲、北美洲等地区,制造业则是中国企业进行投资的主要领域,分别占中国对当地投资的29.6%和21.1%。而在非洲和大洋洲等地区,采矿业则是投资的主要领域(图4)。最后,在对制造业的投资中,劳动密集型产业也不是中国制造业对外投资的重点领域,2018年中国制造业对外投资主要流向了汽车制造业(22.51%)、计算机/通信和其他电子设备制造业(12.41%)和医药制造业(7.17%)。而纺织业、纺织服装/服饰业和家具制造业等传统制造业比重较低,分别占比仅为3.04%、2.09%和2.15%。由此看出,中国企业通过对外投资主动构建的经济全球化并非是劳动密集型制造业的大规模转移,而是优质企业进行海外多样化投资的过程。

图4

图4

2011—2018年中国累计对外直接投资在各大洲及重点投资行业分布

注:数据来源于中国对外投资统计公报。

Fig. 4

Chinese outward FDI stock in each continent during 2011-2018

3.2 战略耦合演变下的路径重构:全球生产网络的深度嵌入

从上文的分析可以看出,中国在经济全球化第三次浪潮中所实现的角色变迁并没有完全按照发达国家给发展中国家预设的梯度转移路线进行,既没有发生像日本、韩国等地区那种由发展型政府主导的崛起过程,也没有出现大规模“以旧换新”的价值链更替。本文认为其背后的原因是中国通过动态调整战略耦合的模式,逐步实现在全球生产网络中的深度嵌入,而这一过程贯穿了中国参与经济全球化第三次浪潮的始终。

在1978年后的改革开放初期,中国政府选择以珠三角为试验区,实施“先行一步”的发展战略。其中最核心的制度设计是以“三来一补”特殊政策框架和经济特区的建设为依托,允许海外资本进入。由此触发港资往内地转移,然后逐步吸引台资、日韩资本,再扩大到欧美资本。在这个过程中,珠三角地区从单纯吸引外商开展“三来一补”生产代工活动,到逐步吸引外资企业整个生产环节,乃至整厂的移植,逐渐走上了外资驱动下的工业化和产业升级之路[32]。这是一种接近于依附式的战略耦合方式,通过提供价格低廉的劳动力、生产资料和其他生产要素,换取跨国公司将低附加值和标准化技术的生产环节,以产业转移或者代工的方式植入珠三角,中国实现了与全球化第三次浪潮的最初对接[33]。在珠三角地区的试验成功之后,中央政府于1986年开始在全国范围内推广珠三角的成功经验[34]。在中央政府的号召下,各地纷纷制定相应的政策以更为开放的制度环境吸引外商直接投资进入。直到2008年,国家正式取消对外资企业的优惠税收政策,依附式的战略耦合模式才宣告退出历史舞台[35,36]。

在依附式耦合退出历史舞台之前,中国并没有一成不变地、被动地接收跨国公司的产业转移,而是同时积极培育多种耦合模式。在20世纪80年代末期珠三角已经经济起飞之时,中国开始实施权力下放的改革,在诸多省的县一级政府下培育乡镇企业,其中以苏南模式最为成功[37]。这些企业一方面依托外资进入所溢出的产业机会(如分包、代工等),同时依托国内市场的逐步开放,通过转移国际上较为廉价或者已经即将被淘汰的成熟生产技术的方式,走向了“代工—引进—消化—吸收”的发展道路,从早期仅从事零部件加工,开始走向整件生产,再逐步升级为外资企业的生产合作伙伴,培育出合作式战略耦合。在此基础上,乡镇企业积极将从外资身上学习到的生产和营销技术应用在国内市场,开启了自创品牌之路,最终培育出一批国内领先企业,例如温州鞋业产业集群[38]和晋江鞋业产业集群[39]的崛起,均是这类模式战略耦合的代表。在这个过程中,国家的宏观政策改革、地方政府的支持,起到了不可或缺的作用[40]。与此同时,以汽车产业为代表的,技术密集型企业集群也在中国政府的培育下出现了互惠式耦合。一方面中国政府依托市场规模优势,设定了保护性产业关税,同时要求进入中国市场的汽车产业的外资企业,必须与国家指定产业开设合资公司,而且每家外资不得与超过两家国企合资,同时设定零部件本地化税率优惠政策,即生产网络本地化越高,税率越低[41]。为了进入中国庞大的汽车市场,外资只能选择遵循国家政策,以“技术换市场”的方式,与中国汽车国企进行互惠式耦合,在此作用下,诞生了北京、上海、广州等一批新的汽车产业集群。互惠式耦合不仅为中国汽车企业带来了庞大的技术转移和升级机会,同时也成为支撑跨国汽车企业持续发展的重要力量,甚至在2008年全球经济危机中,成功挽救了数个汽车巨头免于破产[5]。

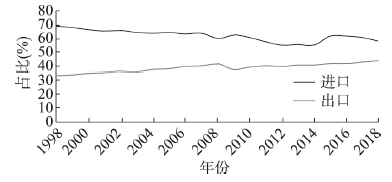

随着多种耦合方式的出现,中国各区域不断加深在全球生产网络中的嵌入,并逐步实现了在全球生产网络中位置的提升[42,43]。一方面中国制造业中间产品的对外依赖逐渐减少。通过与各行业全球领先企业的耦合,中国制造业产业结构逐渐丰富,国内供应链逐渐完善,随着制造业内部供应能力逐渐增强,中国进口贸易中制造业中间产品的占比呈现下降趋势。1998—2018年中国进口贸易中制造业中间产品的占比从69.07%下降到58.12%。另一方面,中国中间产品出口能力不断提升,在全球生产网络中的影响逐渐增强。1998—2018年中国出口贸易中制造业中间产品的比重不断增加,从1998年的33.6%上升到了44.03%(图5)。

图5

图5

1998—2018年中国对外贸易中制造业中间产品占比

注:数据来源于联合国贸易和发展会议(UNCATD)。

Fig. 5

Share of intermediate goods in China's international trade during 1998-2018

表3 1998—2018年中国对外贸易中各行业中间产品占比(%)

Tab. 3

| 年份 | 纺织服装业 | 汽车制造业 | 电子制造业 | |||||

|---|---|---|---|---|---|---|---|---|

| 进口 | 出口 | 进口 | 出口 | 进口 | 出口 | |||

| 1998 | 6.51 | 4.56 | 1.14 | 0.81 | 13.25 | 5.97 | ||

| 2003 | 2.73 | 3.78 | 2.23 | 1.30 | 20.56 | 11.08 | ||

| 2008 | 1.07 | 2.42 | 1.46 | 2.00 | 19.21 | 10.40 | ||

| 2013 | 0.85 | 2.42 | 1.70 | 2.18 | 18.45 | 11.10 | ||

| 2018 | 0.62 | 2.66 | 1.90 | 2.44 | 20.91 | 10.81 | ||

注:数据来源于世界银行。

而在以汽车制造业和电子制造业为代表的的资本密集型和技术密集型产业中,中国中间产品贸易占比都表现出2003年前逐渐增加,2003年后小幅波动的趋势。早期中间产品占比的显著增加表明在参与经济全球化第三次浪潮的初期,大量汽车制造业和电子制造业外商直接投资的进入,使得中国通过发展中间产品加工制造快速嵌入到相关产业的全球生产网络之中。随后呈现出较为规律的波动状态则反映出,中国在资本密集型和技术密集型产业全球生产网络地位的提升过程,不再是简单的此消彼长的生产能力竞赛,而是基于和世界经济相互依赖下的战略耦合模式的动态调整。由于两类行业产品的复杂性,完全依靠国内供应链实现生产是不经济也是不现实的,因此保持和世界适度的相互依赖是相关行业发展升级的必然。在此基础之上,中国企业通过不断调整战略耦合模式,在保持适度外部依赖的同时,逐步开始由加工制造基地向全球重要制造平台的升级[34]。

战略耦合模式的动态调整不仅让中国在全球生产网络中得到了升级发展,还使得中国改变了发达国家给中国预设的定位,也超越了传统产业梯度转移理论所假定的产业发展路径。2008年之后,中国土地成本与劳动力成本逐渐上升,尤其是东部沿海地区。根据传统产业梯度转移理论,生产成本的持续上升会迫使传统产业开始向低成本地区进行整体转移。然而,从中国的实际情况来看,尽管开始出现个别企业外迁的现象,但目前尚未有研究证实已经出现大规模的产业外迁,而且个别外迁到东南亚的企业,主要还是集中在纺织服装等劳动密集型产业。而电子制造业和汽车制造业等产业无论在国家内部还是国家之间都尚未发生大规模转移[44]。这些企业基于中国培育出的生产网络已经扎根于中国的生产要素、供应网络和国内市场之中,其所孕育出的生产环节也已经是各产业全球生产网络的重要组成部分,而不是边缘性加工处理环节。这使得各产业全球生产网络布局在中国的部分具有高度的空间粘性[34, 45]。

企业通过正式和非正式关系建立的网络为企业家带来发展所需的信息和资源,当企业选择外迁时意味着将失去原有的社会网络资本[46]。在这种情境之下,选择外迁会对企业造成巨大的成本损失。因此企业倾向于通过战略耦合模式的动态调整,而不是通过空间迁移的方式来实现升级改进和利润提升。既可以选择与原有合作企业的解耦再与更高层次企业的再耦合,从而实现产业升级[34],也可以选择转向国内市场,依托庞大的国内供销网络实现发展模式的转变[45, 47]。这种战略耦合动态调整的出现,彻底颠覆了西方发达经济体预设的产业转移路径,对发达经济体的战略领先地位形成一定的挑战。一方面,发达经济体转出的企业长期留在中国,将使得双边贸易容易出现逆差,需要寻找新的战略性产品来出口中国,以平衡这个缺口。另一方面,发达经济体的企业大量在中国繁衍,其结果就是大量的资本囤积在中国,这将削弱他们与中国的议价能力,也将削弱他们对其他后发经济体的议价能力[48]。

4 后疫情时期的经济全球化形势与中国道路选择

4.1 后疫情时期经济全球化形势分析

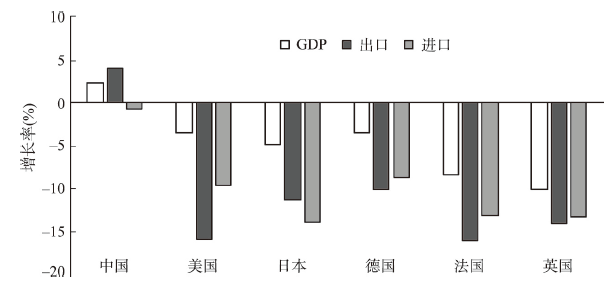

2020年新型冠状病毒肺炎疫情的爆发给全球经济带来巨大冲击。就短期来看,受此次新冠疫情的影响,中国、美国、日本和德国等世界主要经济体的国内经济发展水平和对外贸易水平都受到明显的冲击。根据各国公开的数据显示,2020年世界各主要经济体无论是GDP还是对外贸易总额的增长率都显著下降。值得注意的是,在大部分经济体,新冠疫情对于对外贸易的冲击要显著大于对经济发展的冲击,以美国为例,2020年美国GDP增长率为-3.5%,而进口贸易和出口贸易则分别下降了9.5%和16%。这一情况表明各国当前因防疫隔离的需要,经济发展更多依靠国内生产活动,而对经济全球化的依赖程度有所降低(图6)。长期来看,后疫情时期经济全球化水平将经历一个缓慢复苏过程。若疫情持续肆虐,经济全球化甚至有可能长期陷入“停滞状态”。因此在后疫情时期,全球市场需求将会出现持续性疲软,经济全球化或陷入长期性停滞的格局。但经济全球化的进程并不会由此终结或倒退,而是会出现新的发展轨迹[49]。

图6

图6

2020年各经济体GDP和对外贸易增长情况

注:根据各国公开数据整理。

Fig. 6

The growth rate of GDP and international trade by economy in 2020

就本文重点关注的生产组织领域而言,后疫情时期全球生产网络不会出现大规模的断裂,而是会加速在相对更小尺度的区域层面进行空间重组[49],即区域生产网络的构建进程加快。其实在新冠疫情爆发之前全球生产网络已经呈现出区域化的趋势[50],而此次新冠疫情无疑加速了这一进程[51]。结合实际情况来看,2019年12月美国、墨西哥和加拿大签定“美墨加贸易协定”(United States-Mexico-Canada Agreement)以替代《北美自由贸易协定》,以期通过扩充3国间贸易产品品类和修订贸易规则进一步促进区域生产网络的形成。2020年11月东盟10国及中国、日本、韩国、澳大利亚、新西兰等15国签署了旨在推动亚太地区经贸一体化发展的《区域全面经济伙伴关系》(The Regional Comprehensive Economic Partnership)。这些事实都表明世界各主要经济区都希望加强区域生产网络的建设以此缓冲全球性经济波动带来的震荡[52,53]。因此后疫情时期生产网络的区域化发展将成为经济全球化进程的主旋律。

长期来看,区域生产网络的构建将会推动全球供应链达到新的空间平衡。当前全球供应链虽然已在世界大部分国家完成布局,但是核心零部件的生产依旧高度集中在一些特定国家,例如美国和日本等,而模块集成又主要集中在中国。为避免全球供应链因上述国家生产活动受到全球性波动的影响而陷入系统性瘫痪,未来集成生产可能会加快区域化布局,同时核心零部件的布局范围也会向区域尺度扩大,以期在全球性冲击下运输中断时可以实现区域式响应。在这一趋势下,将可能出现两种并行的趋势。一是发达国家可能降低集成、组装生产对中国的依赖程度,加速中国制造业外移的进程,在制衡中国崛起的同时维护自身国家经济运行的安全性。二是中国凭借新冠疫情期间在疫情防控和复产复工方面的良好表现,进一步吸引全球供应链核心零部件生产环节的迁入。就后者而言,此次新冠疫情期间,中国在疫情防控和复工复产方面的良好表现,使其成为现阶段全球生产能力最稳定的国家,向全球展示了中国已具备稳定的经商环境和较好的经济弹性。因此,后疫情时期中国经济全球化进程所面临的机遇与挑战是并存的[49]。

4.2 后疫情时期中国经济全球化道路选择

随着后疫情时期生产网络区域化进程的逐步深入,部分发达国家或继续加快本国制造业企业向本国及其周边地区回流的速度,这不仅在一定程度上阻碍了中国企业全球扩张的步伐[54],还增加了中国与西方国家“脱钩”的可能。与此同时,部分发展中国家也会因此获益而加速崛起。上述两种情况的同时出现将加剧当前中国进一步参与经济全球化过程中面临的竞争压力。结合中国发展实际来看,当前中国经济已经深度嵌入全球生产网络之中,因此参与经济全球化仍旧是中国未来经济发展的重要途径。在此背景下,中国需要以更主动的姿态——构建国内国际双循环参与到经济全球化的进程之中。

本文认为中国未来可以从以下两个途径构建国内国际双循环:① 在国家内部各地区之间强化国家生产网络,以此加快国内循环的构建,从而为中国提升全球领导力提供必要的保障;② 在坚持高质量融入全球生产网络的同时,加强与周边国家的经贸合作以构建区域生产网络,进一步丰富国际循环的空间内涵。通过缩短生产网络的空间距离,在实现持续享受参与全球分工体系红利的同时削弱全球经济环境波动带来的潜在负面影响。

在构建国内循环的过程中,需要进一步发展国家生产网络。虽然当前国家生产网络已经具备一定的发展基础[55],但整体来看,国内企业在国家生产网络的嵌入程度低于嵌入本地生产网络和全球生产网络的程度[56]。因此,国内循环的构建首先需要促进国内各地区间生产要素的有效流动和生产活动的协作。这不仅需要发挥东部沿海地区在国家发展中引领和资源整合的作用带动内陆各地区发展,还需要充分调动内陆各地区的生产潜力,为东部沿海地区发展提供支持。结合中国区域经济发展历程来看,城市群一直以来都是中国经济发展格局中最具活力和潜力的战略支撑点和增长极点[57],因此在构建和完善国家生产网络的过程中,仍需继续重视和发挥城市群的作用。具体而言,可以将京津冀、长三角、珠三角和成渝等四大城市群作为国家生产网络的顶点,将中原城市群、关中城市群和哈长城市群等其他城市群作为国家生产网络的重要支点,通过共同研发和创新构筑水平合作链以促进四大城市群之间合作,通过产业间的协作分工构筑垂直产业链促进四大城市群与其他城市群之间协同发展,通过“双链叠加”的辐射效应带动其他非城市群地区城市发展,从而使各城市都可以深度嵌入于国家生产网络之中,进而推动国内循环的形成。

在国际循环的深化过程中,中国仍将积极融入全球生产网络之中,但是结合后疫情时期生产网络区域化的发展趋势,未来中国参与国际循环的过程中也需要加强区域生产网络的建设与发展,以此进一步丰富国际循环的空间内涵。在构建区域生产网络时,中国可以直接面向东南亚等周边地区,也可以面向整个“一带一路”沿线国家通过合作开发的形式共同构建区域生产网络。在与上述国家合作共建区域生产网络的过程中,中国的产业发展优势相对明显,全球竞争优势也相对更强,因此中国有机会进入区域生产网络的核心位置。但就现阶段情况来看,中国企业嵌入区域生产网络的过程并不顺利,主要表现为中国企业现有对外投资多未充分考虑相关地区的经济发展需求[58]。因此,未来区域生产网络的构建应该更加强调合作开发和互惠共享,在继续发挥东部沿海地区发展优势的同时,给予内陆地区的城市群更多参与的机会,一方面内陆城市群与周边国家和地区地理邻近,能够更有效便捷地建立经贸合作联系;另一方面内陆城市群与周边地区在产业结构等方面更为相似,可以更好地嵌入到区域生产网络之中[59]。但需要强调的是,全球生产网络的继续融入对于深化国际循环也同样重要。在深度融入全球生产网络的进程中,当前中国参与经济全球化程度较高的四大城市群所起到的引领作用将进一步突出,未来四大城市群应通过深化全球生产网络的嵌入程度,从而获取高端创新知识,提升在全球生产网络中的地位。通过构建区域生产网络和深化全球生产网络,进一步丰富国际循环的空间内涵,全面提升中国的全球领导力。

在构建国内国际双循环的过程中,战略耦合模式的动态调整依旧发挥着重要作用。在发展国内循环时,可将原来在全球生产网络中采取的各类战略耦合模式进行调整并灵活运用于国家生产网络的构建过程中,例如可以结合各地区间的发展梯度势差,也可以依托各产业龙头企业,在国家内部构建“根植性”更强的产业内分工体系。在深化国际循环时,则需要结合不同产业的发展现状及特点,灵活选择战略耦合模式。对于尚未处于国际领先地位的产业,尤其是一些高新技术产业,仍需积极深化国际循环的参与程度,可先通过依附耦合再通过合作耦合和互惠耦合的方式逐步缩小与领先国家的差距。而对于国内发展基础好且深度嵌入全球生产网络的产业,例如汽车制造业和纺织服装业等,可以根据周边国家和地区的具体发展实际,有针对性地采用自主耦合、互惠耦合和合作耦合等方式构建区域生产网络。需要指出的是,未来随着国际循环的不断深入,中国可能会“被动”地面临来自其他国家的主动解耦,因此需要适时调整战略耦合模式,结合国内循环建设,以减少外部发展环境变化可能给中国经济带来的负面冲击。

综上,在后疫情时期,中国应结合国内国际双循环的发展理念,通过战略耦合模式的动态调整构建“全球—区域—国家”多层嵌套型的生产网络,从而实现在充分享受嵌入各尺度生产网络带来益处的同时,还能通过多尺度的生产网络有效缓解潜在全球性危机带来的冲击。

5 结论与讨论

本文从经济地理学视角出发,刻画了经济全球化三次浪潮下世界经济地理格局的演变过程,重新阐释其变动,得到以下两个主要观点:① 全球经济地理格局经历了“核心—边缘”的国家式贸易不均衡阶段,到跨国公司主导的以生产转移为核心的价值链不均衡阶段;继而再从简单的生产迁移到全球生产网络动态重构,进入“网络不均衡”阶段。在这个过程中,发达国家对发展中国家控制和传统产业转移的空间逻辑,是主导世界经济地理格局的变化的主要驱动力。② 中国在经济全球化中的角色随着战略耦合模式的动态调整而不断演变,并改变了由发达国家主导的产业梯度转移发展路径。在融入经济全球化的初期,中国凭借国内市场优势和要素成本优势,以依附式耦合的方式嵌入全球生产网络,实现经济的快速增长。随后在国家经济制度改革和地方政府发展动力释放的影响下,中国培育出多种战略耦合模式,与全球生产网络嵌入的方式不断深化和多样化。当生产要素成本的上升和经济转型压力的“如期而至”时,曾经发生在日韩的产业大规模空间转移没有在中国东部沿海地区出现。已经扎根中国东部沿海的企业不仅没有因生产要素成本的上升而大规模迁出。中国的本土企业通过结合国内市场以及调整战略耦合的方式,逐渐实现本地升级,并逐步走向海外扩张的路线,让中国成为经济全球化主导力量中的一员。

中国在未来经济全球化进程中影响力的提升需要进一步发挥地理腹地优势,动态调整参与“全球—区域—国家”生产网络的战略耦合模式,着力构建国内国际双循环。一方面通过构建国家生产网络打造国内循环为提升全球竞争力提供保障,另一方面中国仍需坚持参与国际循环,并通过积极构筑区域生产网络丰富国际循环的空间内涵,以实现持续享受经济全球化红利的同时减缓潜在全球经济动荡带来的冲击。具体而言,当前中国东中西部各地区间在全球产业分工体系中的地位存在明显的梯度势差[60],未来中国可以利用各地区间参与全球化水平的差异,巧妙吸收不同类型的外商直接投资,实现对全球生产网络多环节的综合承接。其中,东部地区的京津冀、长三角、珠三角以及西部地区的成渝城市群等重点区域应利用当前深度参与经济全球化的基础,继续加强与全球创新网络和全球研发网络的合作,进而引领国家生产网络的建设和助力中国向全球生产网络的研发环节继续攀升。而在中西部大部分地区应该仍以承接和发展制造环节为主,在进一步激发中西部地区市场活力和要素潜力的同时为东部地区提供支持,这样既符合相应区域的比较优势又有助于完善国家生产网络。

在新阶段的经济全球化中,“互利共赢”和“开放包容”将成为各国政府的普遍诉求,而这两点正与“一带一路”倡议中的“丝路精神”高度契合[6]。可以预见,在“一带一路”倡议下,通过动态调整在“全球—区域—国家”生产网络中战略耦合模式所打造的国内国际双循环在提升中国全球影响力中的积极作用将被进一步放大。因此,如何有机结合“一带一路”倡议提供的制度空间红利和国内国际双循环的空间内涵,将成为中国未来经济全球化发展的关键,也为未来中国经济地理学研究提供了新的方向。

参考文献

Review of regional spatial restructure under economic globalization

经济全球化下的区域经济空间结构演化研究评述

Interpretation of economic spatial structure evolution tendency under globalisation

全球化下经济空间结构演化趋势的解析

Reconstruction of economic and trade rules in the changing situation of economic globalization and China's countermeasures

经济全球化变局、经贸规则重构与中国对策: “全球贸易治理与中国角色”圆桌论坛综述

China's Belt and Road Initiative: Changing the rules of globalization

DOI:10.1057/s41267-019-00283-z [本文引用: 1]

The dynamics of local upgrading in globalizing latecomer regions: A geographical analysis

DOI:10.1080/00343404.2016.1143924 URL [本文引用: 5]

Discursive construction of the Belt and Road Initiative: From neoliberal to inclusive globalization

DOI:10.18306/dlkxjz.2017.11.001

[本文引用: 3]

There is an increasing international consensus that the Belt and Road Initiative (BRI) affords a platform for increasingly more countries to explore new international economic governance mechanisms and new development paths. In the meantime, neoliberal globalization has arrived at a crossroads, while anti-globalization voices are louder and practices more frequent since the 2008 global financial crisis, challenging the future of globalization at the scale of the world as a whole. Against this background, political elites and scholars increasingly see the BRI as a possible alternative and new globalization path and, in particular, as a path towards inclusive globalization. Based on a brief review of the process and mechanisms of global economic expansion, and a critique of neoliberal globalization, this article tries to use the vision and actions proposed by the BRI to develop the concept of inclusive globalization. The article suggests that inclusive globalization involves at least the following dimensions: a better and more powerful role of state as a mediator to ensure social justice and stability; correcting the duration mismatch in financial markets and provision of more patient capital to finance infrastructure development, productive activities, and real services in economically less-developed countries and regions; encouraging countries to choose and experiment with development paths that best fit their national conditions and values; enabling all stakeholders to participate equally in globalization; and protecting cultural diversity while promoting economic globalization. Although these dimensions are not sufficient to delineate in detail inclusive globalization, they at least point to several directions for future research on the topic and may offer some support for discursive construction of the BRI.

“一带一路”倡议的理论建构: 从新自由主义全球化到包容性全球化

Vertical specializing: Trade and production pattern during economic globalization

垂直专业化: 经济全球化中的贸易和生产模式

Analysis of value chain optimization based on corporation's capability under the background of economic globalization

经济全球化下基于企业能力的价值链优化分析

Globalization: Countries, cities and multinationals

DOI:10.1080/00343404.2010.505915 URL [本文引用: 1]

Global Shift: Mapping the Changing Contours of the World Economy

Deglobalization movements and globalization transition

逆全球化风潮与全球化的转型发展

China and the economic globalization

中国与经济全球化

Rising powers and the drivers of uneven global development

DOI:10.1080/23792949.2016.1227271 URL [本文引用: 1]

Time and spatial transformation of economic globalisation in the Yangtze River Delta region

长三角区域的经济全球化进程的时空演化格局

Estimating China's manufacturing export quality: Pitfalls and remedy

中国制造业出口质量的准确衡量: 挑战与解决方法

Global value chains position and regional industry upgrading policies: Taking Northeast China as an example

DOI:10.13249/j.cnki.sgs.2016.09.010

[本文引用: 1]

This article applies input-output analysis method to measuring the global value chain position of Northeast China’s industries. We find that in the northeast of China, the mining and other basic industries have a large amount of value-added in trade, but are faced with the threats of excess capacity and low-end locking. While the status of manufacturing industries is relatively low in trade, these industries show an obvious comparative disadvantage that tends to deteriorate. In terms of specific province in Northeast China, the overall level of industrial technology and status in Liaoning Province is higher, whose disadvantage in the mining is relatively small, the disadvantages of Jilin Province in the manufacturing industry is larger, and Heilongjiang Province has an average level of industrial value chain position, but has a more serious excess capacity and low-end locking risk in the mining. Therefore, in order to upgrade the global value chain position of Northeast China, we need to transform the traditional principle of industry development and foreign trade, strengthen the construction of innovation ability and combine information technology with traditional industry to realize a new industrial pattern and innovation-driven intensive development.

全球价值链下区域分工地位与产业升级对策研究: 以东北三省为例

Catching-up and post-crisis industrial upgrading: Searching for new sources of growth in Korea's electronics industry

Study of global spatial relationship between financial and manufacturing sectors: Based on global 500 largest corporations of Fortune

全球金融业与制造业的空间分布关系: 基于《财富》500强企业的实证分析

Encore for the enclave: The changing nature of the industry enclave with illustrations from the mining industry in Chile

DOI:10.1111/ecge.2015.91.issue-2 URL [本文引用: 1]

Globalisation and urban transformations in the Asia-Pacific region: A review

DOI:10.1080/0042098002302 URL [本文引用: 1]

The governance of global value chains

DOI:10.1080/09692290500049805 URL [本文引用: 1]

A review on the study of the embed barriers and upgrade dilemma of the global R&D network

DOI:10.2307/142020 URL [本文引用: 1]

全球研发网络嵌入障碍及升级困境问题研究述评

Globalization, trade liberalisation and the issues of economic diversification in the developing countries

Global modularity of services multinationals and services international transfer as well as the significance to China

服务型跨国公司全球模块化与服务业国际转移及其对中国的启示

Institutions, Industrial Upgrading, and Economic Performance in Japan: The 'Flying-Geese' Paradigm of Catch-up Growth

Local Dynamics of Industrial Upgrading: The Case of the Pearl River Delta in China

The reasons, effects and countermeasures of the continuous decline of foreign direct investment in China's manufacturing industry

中国制造业外商直接投资持续下降的原因、影响和对策

Economic globalization, global financial crisis and China: A financial geography perspective

DOI:10.18306/dlkxjz.2019.10.004

[本文引用: 1]

The impact of the 2008-2009 global financial crisis on Western developed countries, especially the Anglo-American economies, is far-reaching and is reflected on economic, political, and social dimensions. A large body of scholars from various disciplines has attempted to explain the outbreak of the financial crisis. This study analyzed the relationship between economic globalization and the global financial crisis, and explored the impact of the crisis on China from a financial geography perspective. First, this study examined the formation of a new international labor division in the context of economic globalization, identified the transmission dynamics of the financial crisis, and mapped the changing geographies of world economies shaped by the financial crisis. With regard to China, the global financial crisis was external. The economic recession and consumption contraction of Western developed countries have directly affected China's exports, but the financial crisis has not fundamentally affected China's financial system. Second, the article explains why the global financial crisis did not impact China's financial system. The spatial heterogeneity of institutions, the varieties of market economic systems, the government's positive role and control, and China's banking-dominant financial system were all important contributors. Third, the interests of Chinese and international financial geographers on China have gradually increased in the last decade and this article summarizes the latest research progress and identifies the shortcomings of the existing research. Finally, based on the research progress of Western financial geography, this article puts forward some suggestions for the construction of China's financial geography in the future.

经济全球化、全球金融危机与中国: 基于金融地理学的视角

Regional development and the competitive dynamics of global production networks: An east Asian perspective

DOI:10.1080/00343400902777059 URL [本文引用: 1]

Theoretical thread and problems of strategic coupling

战略耦合的研究脉络与问题

Progress of relational economic geography: Whether theorizing China's experiences

关系经济地理的研究脉络与中国实践理论创新

Regional powerhouse: The greater Pearl River Delta and the rise of China

DOI:10.1111/j.1467-8306.2006.00517_9.x URL [本文引用: 1]

Foreign-investment-induced exo-urbanisation in the Pearl River Delta, China

DOI:10.1080/0042098975961 URL [本文引用: 1]

Strategic coupling and industrial upgrading in the Pearl River Delta: A global production network perspective

全球生产网络视角下珠三角区域经济的战略耦合与产业升级

Locational distribution and spatial diffusion of Hongkong-Macao's FDIs in China

港澳地区对中国内地直接投资的区位选择及其空间扩散

Spatio temporal patterns and location factors of FDI in China,

中国外商投资区位选择的时空格局与影响因素

Beyond the Sunan model: Trajectory and underlying factors of development in Kunshan, China

DOI:10.1068/a3567 URL [本文引用: 1]

Upgrading Chinese local clusters in the context of global shift: With special reference to Wenzhou's footwear cluster

全球鞋业转移背景下我国制鞋业的地方集群升级: 以温州鞋业集群为例

Going public and industrial upgrading of traditional clusters in developing countries: Rethinking the dynamics of the 'Jinjiang Model' in China

Transnational corporations and 'obligated embeddedness': Foreign direct investment in China's automobile industry

DOI:10.1068/a37206 URL [本文引用: 1]

Urban globalization process of China's cities since the early 1980s

DOI:10.11821/xb201010001

[本文引用: 1]

Cities have been greatly influenced by the wave of globalization during the past half century, which has made the World City and Global City into a world popular research heat topic. Most existing research has focused on the about 50 cities on the top of the world city system before the end of the 1980s, only very recently extended to the 220 major cities, while most cities in the developing countries are neglected out of the World City Map. Regarding the driving forces of the World City/Global City, the economic function, particularly the producer services of these cities at the global level, in which the roles transnational corporations play, have been over emphasized. The questions are naturally and automatically arising: Are the other cities besides the top ones influenced by globalization? Are those average cities also experiencing the process of globalization? In which ways and at what levels are those general cities globalizing or globalized? In order to seek answers to these questions, Taking all the cities in China at prefectural level and above as research objects, we constructed an evaluation indicator system, and explored the change of the urban globalization levels of each Chinese city based on the data covering the years of 1984, 1990, 1995, 2000, 2004 and 2007. We found that: (1) all China's cities has witnessed the rise of their urban globalization levels during the last more than 2 decades. (2) The major cities such as Shanghai, Beijing, Shenzhen and Guangzhou have seen the most rapid development of urban globalization. So not only the world top cities but also the average Chinese cities have been experiencing the process of globalization. We have also found that manufacturing function has been a very important driving force of many world factory cities in the course of their globalization process in China.

改革开放以来中国城市全球化的发展过程

Participation in global production networks and export product upgrading

DOI:10.11821/dlxb201708001

[本文引用: 1]

<p>Organized globally and led by trans-national enterprises, global production networks (GPNs) develop rapidly along with the advancement of technology and deepening of trade liberalization. GPN provides great opportunities for developing countries to blend in global economy and realize their technological advance, as well as value chain upgrading. Facing the pressure of shifting model of economic development, China has urgent need of optimizing export trade though she has experienced marvelous success especially on export trade during the past few decades, so that the study on export product upgrading can be particularly important. Based on such consideration, this article focuses on how participating GPN influences China's export product upgrade. This article uses the conception of quality to quantitively describe product upgrade, and we calculate the product quality based on data of customs trade database from 2000 to 2011. The result shows that export product quality presents a declining trend from east to west of China, and the average quality of the whole country fluctuates a lot during 2000-2011 with a slight rising trend showing up recently. We then build several econometric models to examine whether participating in GPN matters, and how exactly this influence works. The results show that participating in GPN has remarkable influence on export product upgrading especially in eastern China, but market dispersion does not help in product upgrading. We also find that R&D investment cannot promote regional position in global value chain in eastern China, forming a typical "Low-end lock-in". Capital- and technology-intensive products benefit a lot from participating in GPN while labour-intensive exports may open markets with low-quality products. Fiscal decentralization is a key determinant in eastern and central provinces, and local governments tend to give more support to technology-intensive product upgrading.</p>

参与全球生产网络与中国出口产品升级

The transfer of manufacturing industry among eight regions in China: Based on the idea of shift-share analysis

DOI:10.2307/142573 URL [本文引用: 1]

中国制造业八大区域转移分析: 基于偏离—份额分析

Market reorientation and industrial upgrading trajectories: Evidence from the export-oriented furniture industry in the Pearl River Delta

DOI:10.11821/dlyj201807016

[本文引用: 2]

In the aftermath of the 2008 global financial crisis, export-oriented industries in China have engaged in the transition from exports to focusing on both exports and domestic sales. However, the impact of market reorientation on industrial upgrading of manufacturing firms remain understudied. Drawing upon the global production networks (GPNs) perspective, this study explores the upgrading trajectories of export-oriented firms in their market reorientation towards China's market. This paper takes the export-oriented furniture industry in the Pearl River Delta (PRD), China as a case. On the basis of in-depth interviews, results suggest that furniture firms are strategically coupled with China's domestic market by establishing networks relations, intra-firm coordination relations, and market-based relations with domestic agents. Market reorientation has stimulated variegated upgrading trajectories of furniture firms. Some furniture firms gained functional upgrading opportunities, while some experienced industrial downgrading. The research on industrial upgrading in the market reorientation could enrich the literature by exploring the implications of the rise of emerging markets in the post-crisis era. It also helps to understand the transformation of export-oriented industries in China in the contemporary global economy.

市场转向与产业升级路径分析: 以珠江三角洲出口导向型家具产业为例

Geographical dynamics and industrial relocation: Spatial strategies of apparel firms in Ningbo, China

DOI:10.1080/15387216.2013.849402 URL [本文引用: 1]

Turkishization of a Chinese apparel firm: Fast fashion, regionalisation and the shift from global supplier to new end markets

DOI:10.1093/cjres/rsv009 URL [本文引用: 1]

Spatial-temporal evolution of China's export-oriented foreign-funded enterprises' products from the perspective of trade protection

贸易保护视角下中国出口导向型外资企业产品演化

The impacts of COVID-19 pandemic on the development of economic globalization

DOI:10.11821/dlyj020200514

[本文引用: 3]

The COVID-19 pandemic is considered the biggest crisis confronted with the world after the Second World War, which has brought huge impacts on people’s health and daily life, economic growth and employment as well as national and international governance. Increasing pessimism is buzzing among scholars, critics, entrepreneurs, the mass and even government officials, and views like the end of economic globalization, large-scale spatial restructuring of global supply chains and fundamental change of the world economic governance structure are becoming prevailing on the media. This paper tries to address the issue of the development trend of economic globalization in the post-pandemic era by developing a framework of globalization’s Triangle Structure to understand its dynamics in addition to a summary of the on-going impacts of the COVID-19 pandemic. We argue that the spatial fix of capital accumulation, time-space compression led by technological advance and openness of nations are the three major drivers of economic globalization, and the changes and interactions of these three drivers decide the development trend of economic globalization. From such a dynamic viewpoint, economic globalization is an ever-changing integration process without an end but constant fluctuations. The cost of decoupling of nations from globalization would be very huge because they have been highly integrated by global production networks and trade networks and no nation can afford a complete decoupling. The so-called de-globalization phenomena are just short-term adjusting strategies of nations to cope with power reconfigurations brought by economic globalization. The pandemic will have little impacts, or probably nothing, on the spatial fix of capital accumulation and time-space compression led by technological advance, but may temporarily influence some nations' openness. If the pandemic does not last long, economic globalization will resume from the shock soon after the world goes back to normal, and develop and restructure according to its own dynamics. Thus, we tend to believe the pandemic at most slams the brake of globalization and would not be able to put it into reverse. Economic globalization will not stop or reverse, but develop towards a more inclusive stage.

新冠肺炎疫情对经济全球化的影响分析

Supply-chain trade: A portrait of global patterns and several testable hypotheses

DOI:10.1111/twec.12189 URL [本文引用: 1]

From globalization to regionalization: The United States, China, and the post-Covid-19 world economic order

DOI:10.1007/s11366-020-09706-3 URL [本文引用: 1]

Supply chain contagion and the role of industrial policy

DOI:10.1007/s40812-020-00167-6 URL [本文引用: 1]

Reshaping the policy debate on the implications of COVID-19 for global supply chains

DOI:10.1057/s42214-020-00074-6 URL [本文引用: 1]

China's challenge: Geopolitics, de-globalization, and the future of Chinese business

DOI:10.1017/mor.2019.49 URL [本文引用: 1]

Domestic reginal value chain, global value chain and regional economic growth

国内区域价值链、全球价值链与地区经济增长

Industry-regional characteristic of China's manufacturing embedded into national value chain and global value chain

中国制造业嵌入国家价值链和全球价值链的产业—区域特征

The formation, development and spatial heterogeneity patterns for the structures system of urban agglomerations in China

中国城市群结构体系的组成与空间分异格局

Spatial pattern of Chinese outward direct investment in the Belt and Road Initiative area

中国对“一带一路”沿线直接投资空间格局

Impacts of the Belt and Road Initiative on the spatial pattern of territory development in China

DOI:10.11820/dlkxjz.2015.05.002

[本文引用: 1]

The "Belt and Road Initiative" is and will continue to be an overall strategy of China's all round opening-up for a long time into the future. The building of the "Belt and Road" has become a long term national strategy for China, which will have great impacts on the spatial pattern of China's territory development. Based on an analysis of the current characteristics of the spatial pattern of China's territory development, this study examines the influence of the "Belt and Road Initiative" on the spatial pattern of China's territory development with regard to the all round opening-up, improvement of facilities connectivity, changes of energy supply system, trade, and social and culture exchanges. The "Belt and Road Initiative" emphasizes international facilities connectivity and all-dimensional opening-up including in the coastal, border, and inland areas. Based on the great international transport and economic corridors proposed by the Chinese government in the "Vision and Action on Jointly Building Silk Road Economic Belt and 21st-Century Maritime Silk Road," this article mainly analyzes the impacts of different international economic corridors on territory development in different regions. The main results are as follows. (1) The "Belt and Road Initiative" will have great impacts on the spatial pattern of China's territory development. Although different international economic corridors influence different regions, the western region of China will benefit the most from the "Belt and Road Initiative", which conduces to shape an equitable territory development. (2) The "Belt and Road Initiative" will facilitate the formation of several metropolitan economic areas and economically highly developed areas in the inland area that open to the outside, such as Xi'an, Chengdu, Chongqing, Urumqi, Kunming, Nanning, Wuhan, Zhengzhou, and so on. These areas will form an all round opening-up territory development pattern. (3) The "Belt and Road Initiative" will provide more economic hinterland for the coastal areas' industrial structure upgrading and economic development, which will strengthen the coastal areas' international competitiveness and help to form a high efficiency territory development pattern. (4) The "Belt and Road Initiative" will accelerate the development of port of entry and inland border cities, such as Dongxing, Ruili, Manzhouli, Erenhot, Khorgas, and promote the development of cross-border economic cooperation areas based on successful implementation of the Khorgas cross-border economic cooperation area, which will drive the development of border areas that will become an important region for territory development.

“一带一路”战略对中国国土开发空间格局的影响

Network structure evolution and the spatial-temporal pattern of China western cities participating in global and national competition

中国西部城市参与全球和全国竞争的时空格局及网络结构演化

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}